70 Cart & Checkout UX Articles

These articles are based on observations and test findings from our usability research on cart and checkout.

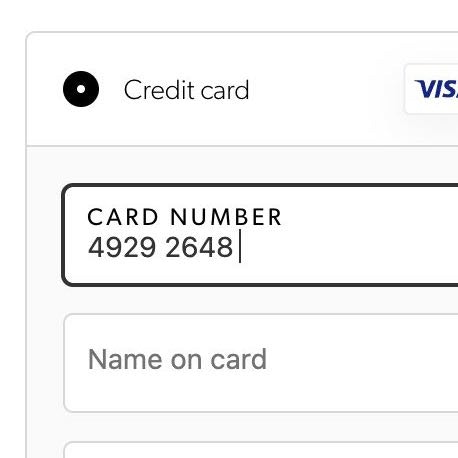

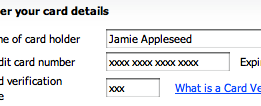

The ‘Credit Card Number’ Field Must Allow and Auto-Format Spaces (80% Don’t)

15% of sites don’t actively aid users in typing their 16-digit card number by autoformatting it with spaces. Learn why it's so important.

Featured

Checkout UX 2025: 10 Pitfalls and Best Practices

November 25, 2025 (Updated)Popular

Ecommerce Gifting UX: 4 Ways to Provide a Superior Gifting UI and Flow

November 20, 2025 (Updated)Popular

10 Cyber Monday UX Best Practices

September 16, 2025 (Updated)Popular

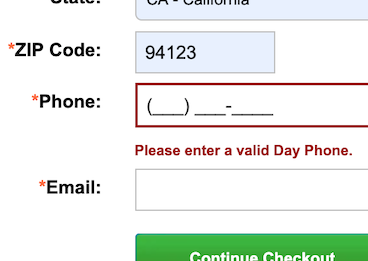

Phone Number UX: Always Explain Why the “Phone Field” Is Required (39% Don’t)

July 29, 2025 (Updated)Popular

4 “Online Grocery” Ecommerce UX Best Practices

July 15, 2025 (Updated)Popular

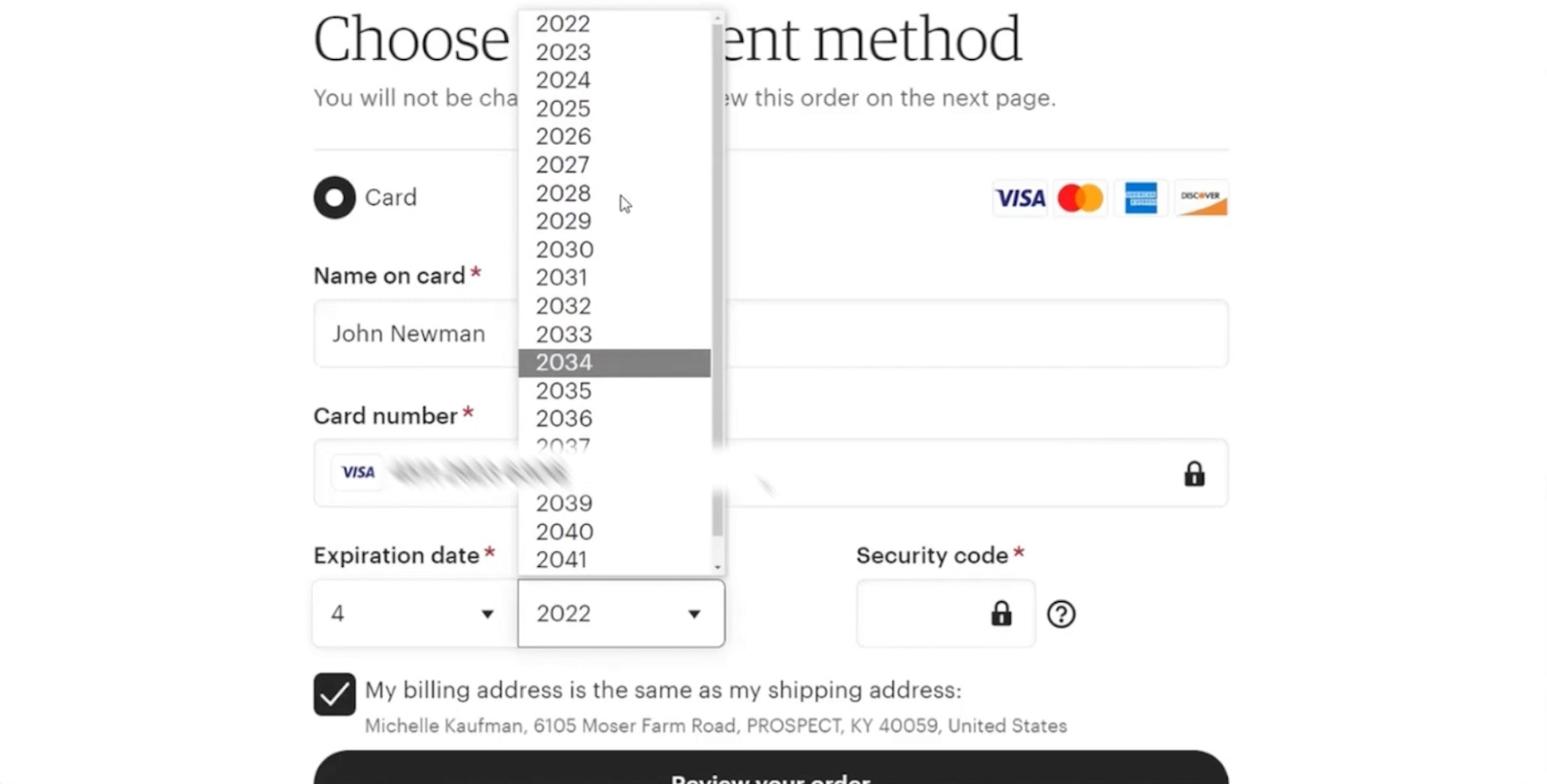

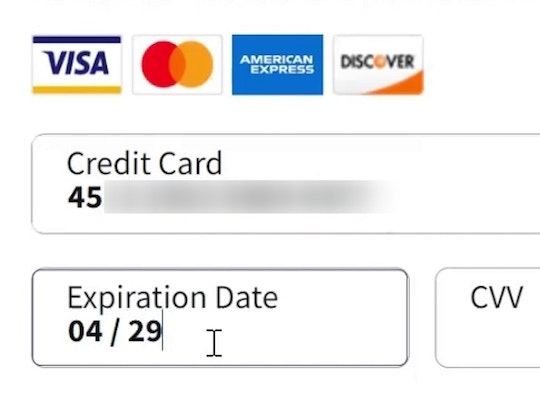

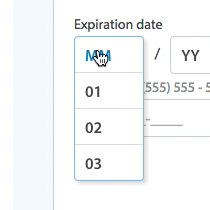

Format the “Expiration Date” Fields Exactly the Same as the Physical Credit Card (72% Don’t)

Our UX testing found that difficulty inputting their credit card expiration date needlessly delayed users from placing orders — yet 72% of sites fail at this. See our latest Checkout findings.

Featured

The ‘Credit Card Number’ Field Must Allow and Auto-Format Spaces (80% Don’t)

June 5, 2025 (Updated)Popular

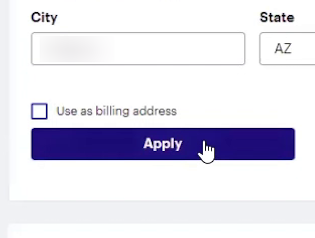

Checkout UX: Avoid “Apply” Buttons for Most Fields (22% of Sites Don’t)

May 14, 2025 (Updated)Popular

4 Ways to Improve UX for Ecommerce Mass Merchant Sites

April 29, 2025

5 Best Practices for Communicating Sustainability in Ecommerce

April 22, 2025 Popular

4 Ways to Improve the Post-Checkout UX

March 25, 2025

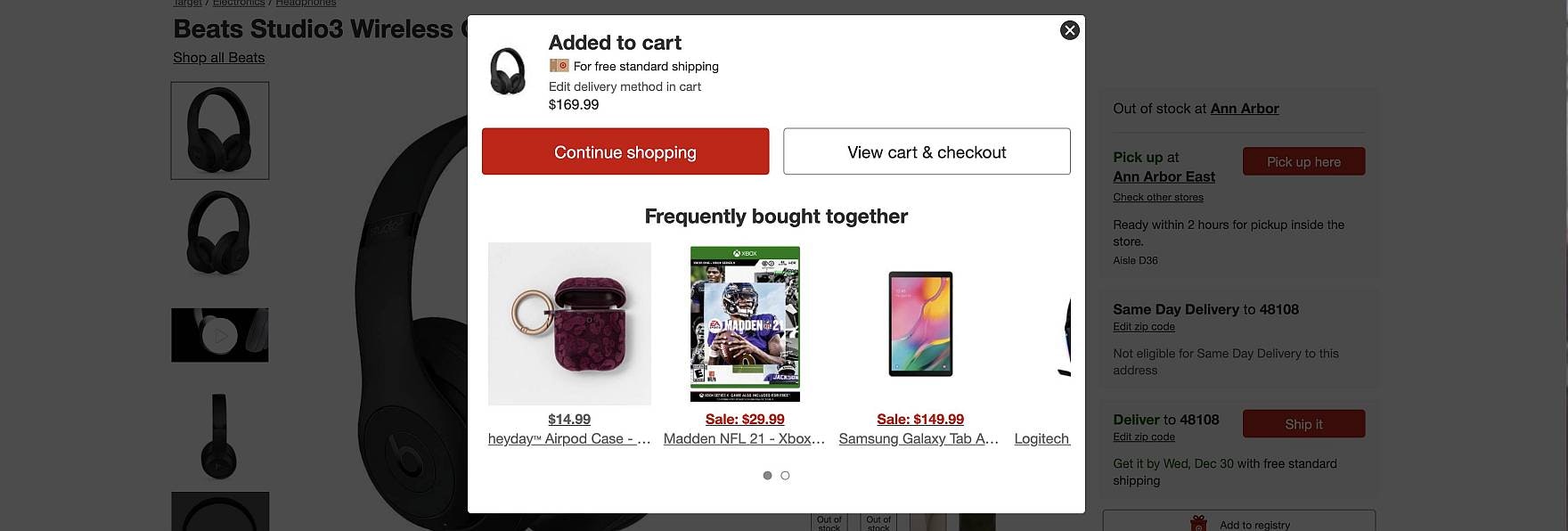

6 Ways to Improve the Relevance of Cross-Sells in the Cart (52% of Desktop Sites Don’t Do Enough)

Our large-scale usability testing reveals that product recommendations and offers that appear unrelated to the user’s cart contents erode confidence in the site and its recommendations — even relevant ones.

Featured

Desktop UX Trends: 10 Common Pitfalls & Best Practices

March 6, 2025 Popular

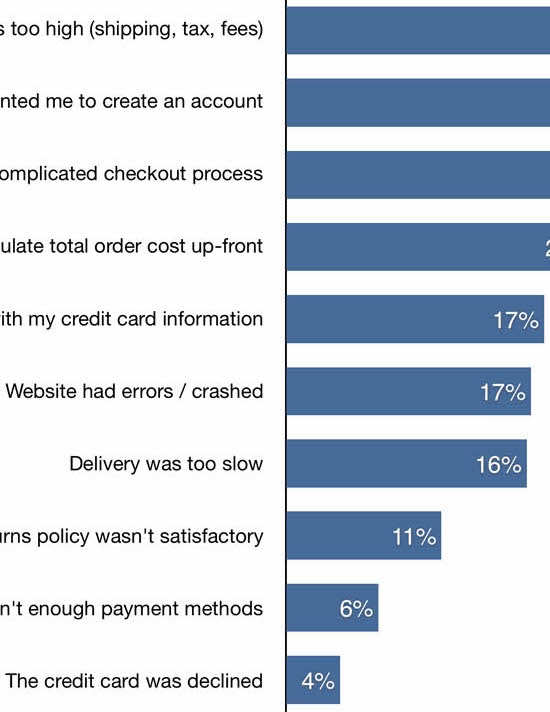

Reasons for Cart Abandonment – Why 70% of Users Abandon Their Cart (2025 data)

February 2, 2025 (Updated)Popular

Drop-Down Usability: When You Should (and Shouldn’t) Use Them

January 28, 2025 (Updated)Popular

Checkout Optimization: 5 Ways to Minimize Form Fields in Checkout

June 26, 2024 Popular

2024 E-Commerce Checkout: Expanded and Updated Checkout Research Findings

March 13, 2024

Checkout Optimization: 5 Ways to Minimize Form Fields in Checkout

Checkout optimization: the average number of form fields in checkout is 11.3 — and 22% of users have abandoned due to checkout complexity. See how to reduce form fields to optimize checkout.

Featured

Retain Data in Sensitive Credit Card Fields after Validation Errors (34% Don’t)

February 6, 2024

Usability Testing of Inline Form Validation: 31% Don’t Have It, 4% Get It Wrong

January 9, 2024 Popular

Improve Validation Errors with Adaptive Messages (98% Don’t)

December 14, 2023 Popular

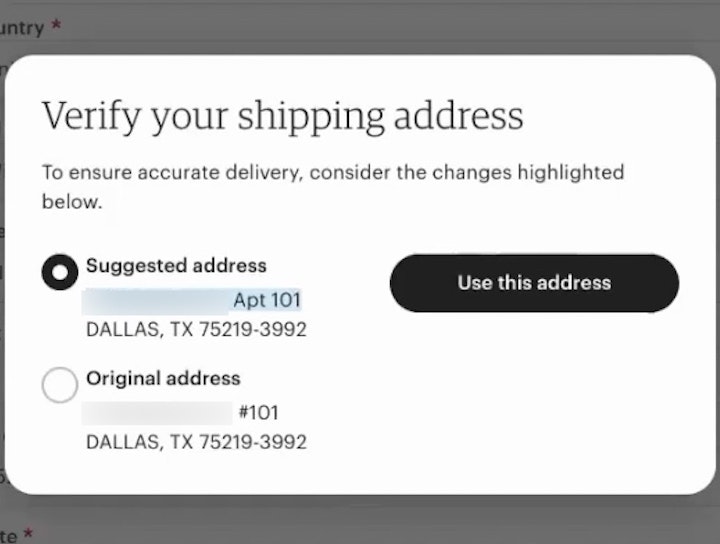

Have an Address Validator (47% Don’t)

November 28, 2023

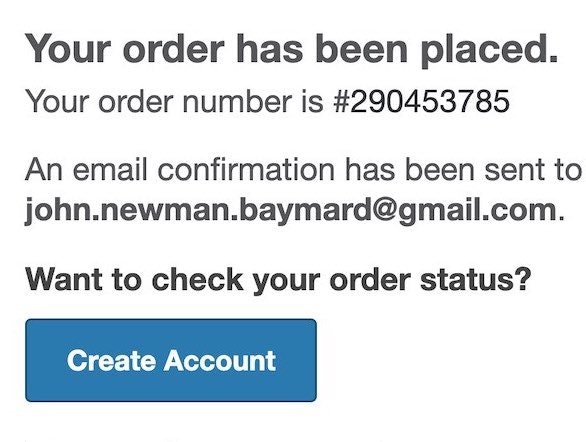

6 Ways to Get More Out of Your Order Confirmation Page

November 8, 2023 Popular

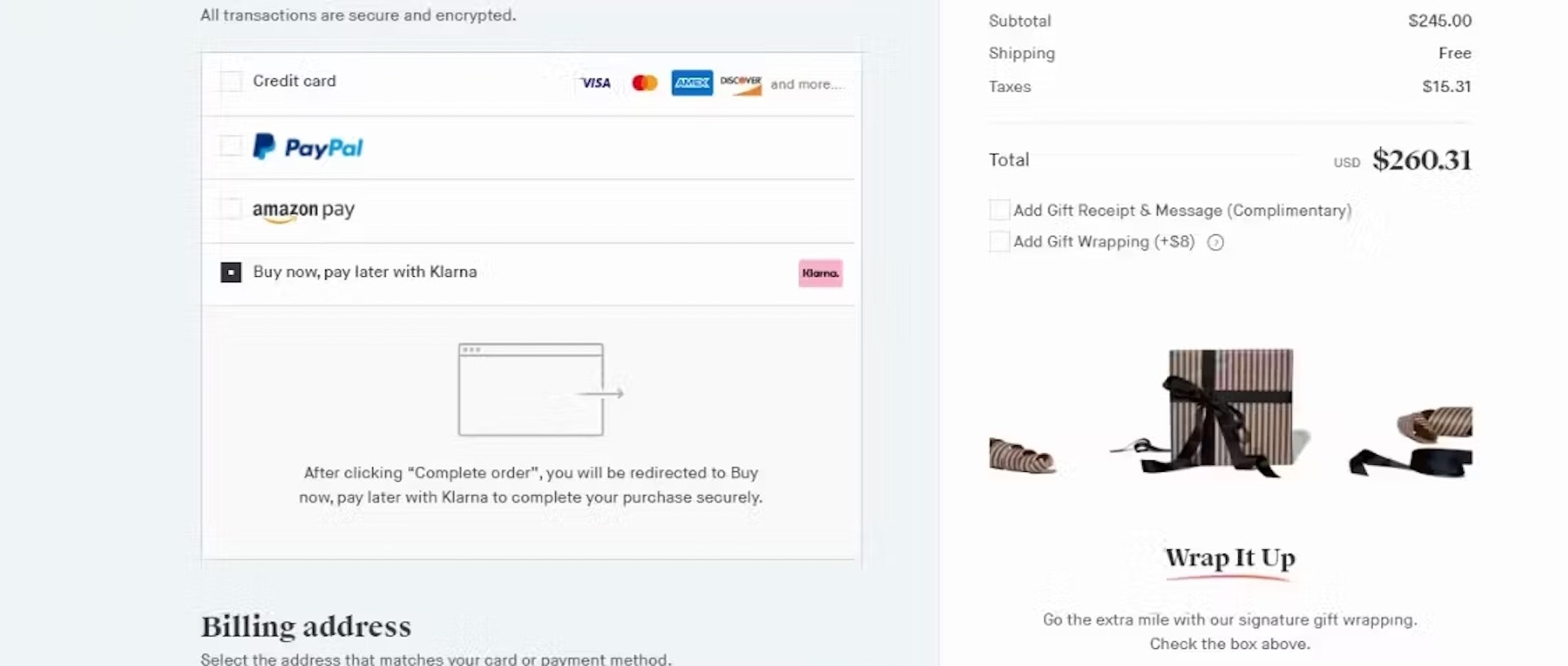

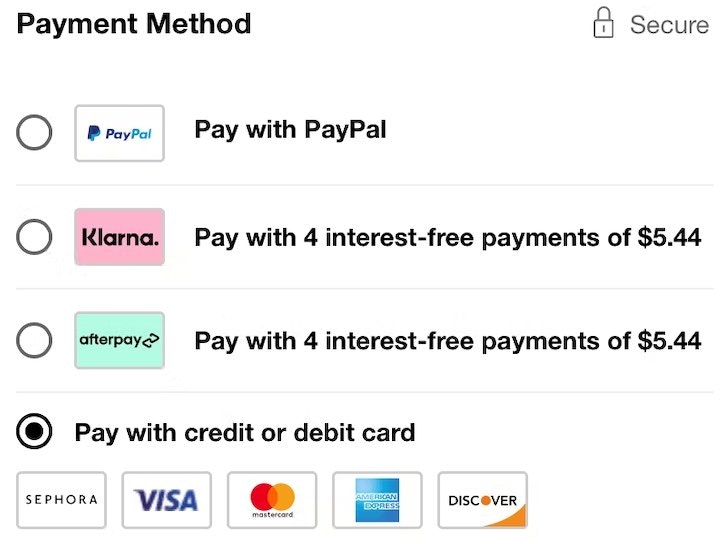

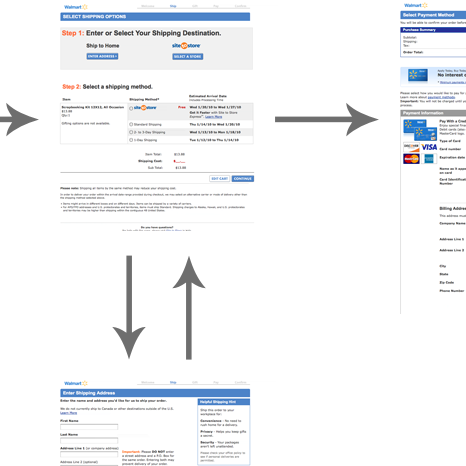

Payment Method UX: Designing Payment Selection

A subgroup of users relies on third-party payment options to complete their checkout — yet 21% of sites only accept 1 method. See our latest test findings on payment method UX.

Featured

Form Field Usability: Avoid Extensive Multicolumn Layouts (16% Make This Form Usability Mistake)

October 31, 2023 Popular

Format the “Expiration Date” Fields Exactly the Same as the Physical Credit Card (72% Don’t)

October 3, 2023 Popular

Always Collapse Completed Accordion Checkout Steps into Summaries

September 27, 2023 Popular

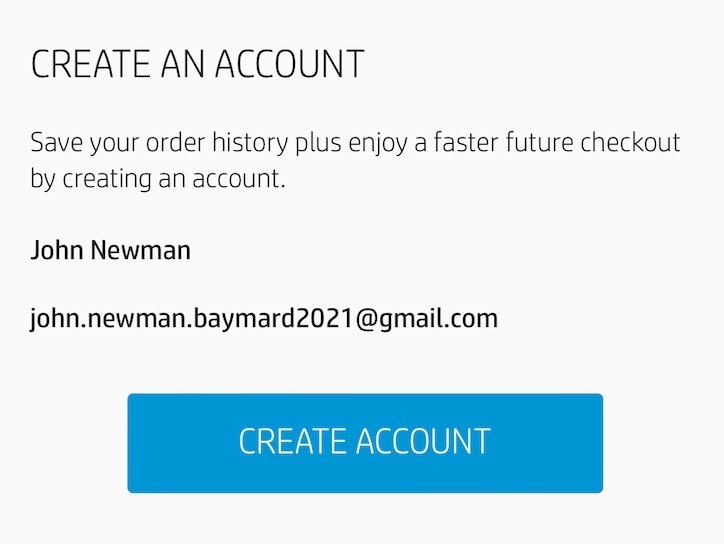

Save Account Creation for the Confirmation Step (42% Don’t)

September 19, 2023 Popular

Payment Method UX: Designing Payment Selection

September 5, 2023 Popular

Checkout UX 2025: 10 Pitfalls and Best Practices

In Baymard's latest benchmark of 180+ leading ecommerce sites, 64% performed "mediocre" or worse in Checkout UX. Here are 10 common Checkout UX pitfalls and strategies for improving Checkout UX.

Featured

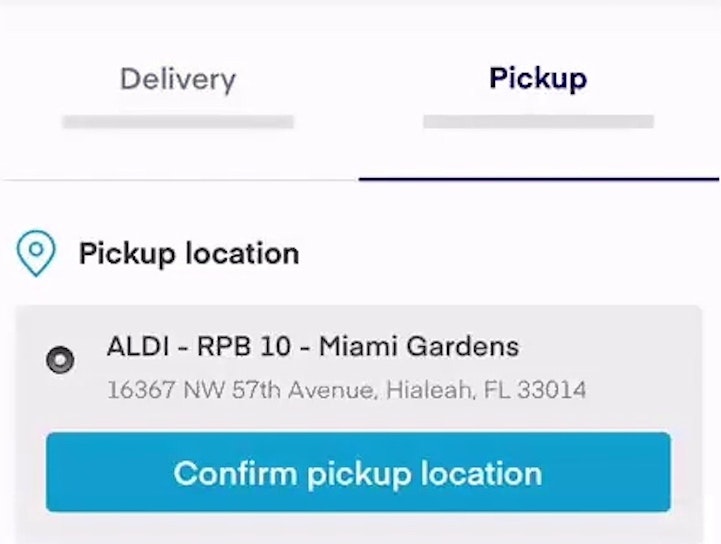

Include All Order-Fulfillment Options in the Fulfillment-Selector Interface (50% Don’t)

July 6, 2023

Use “Delivery Date” Not “Shipping Speed” (41% Don’t) — From UX Research to Implementation Roadmap

June 27, 2023

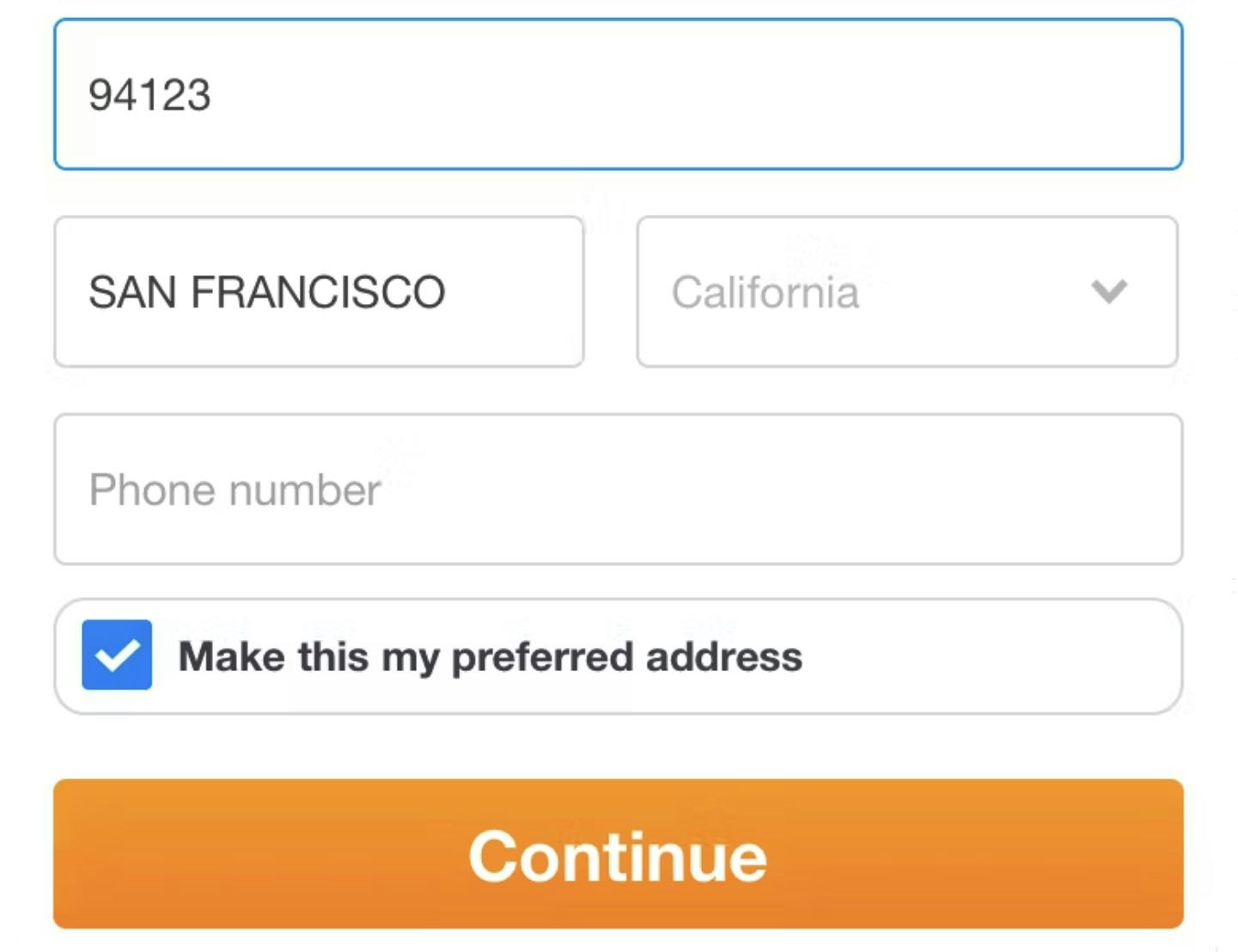

Checkout Usability: Autodetect “City” and “State” Inputs Based on the User’s Postal Code (28% of Mobile Sites Don’t)

April 11, 2023

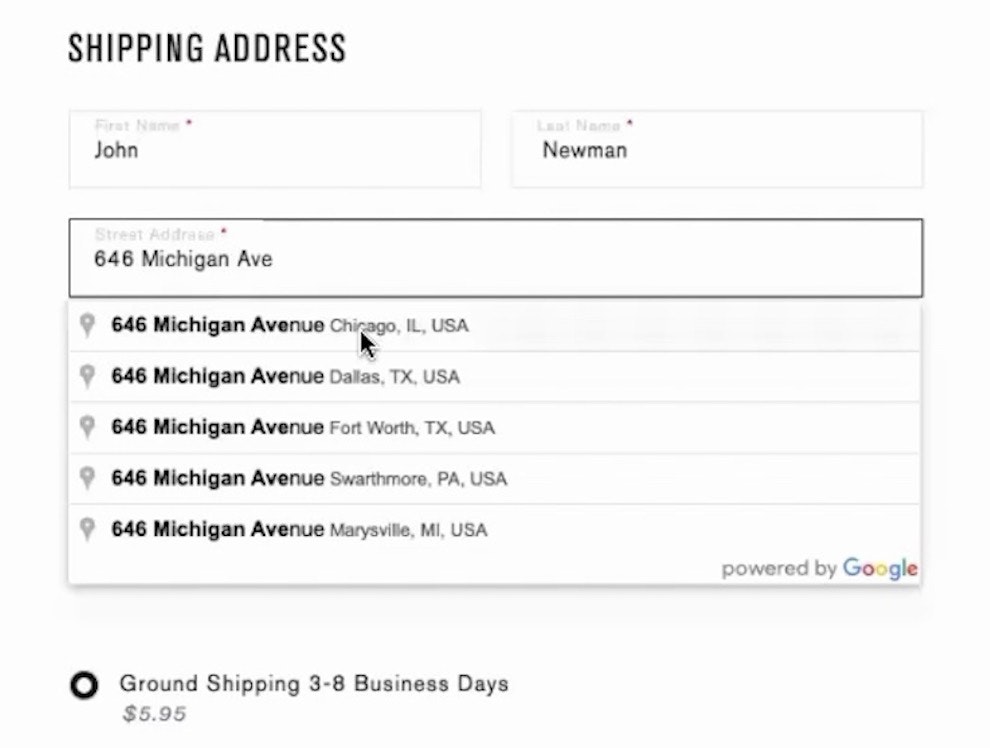

Provide a “Fully Automatic Address Lookup” Feature (55% Don’t)

March 24, 2023

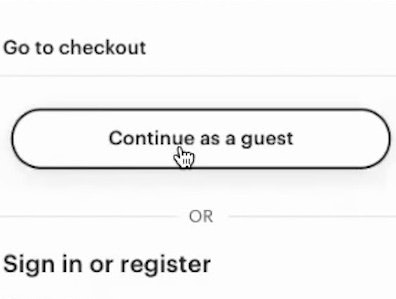

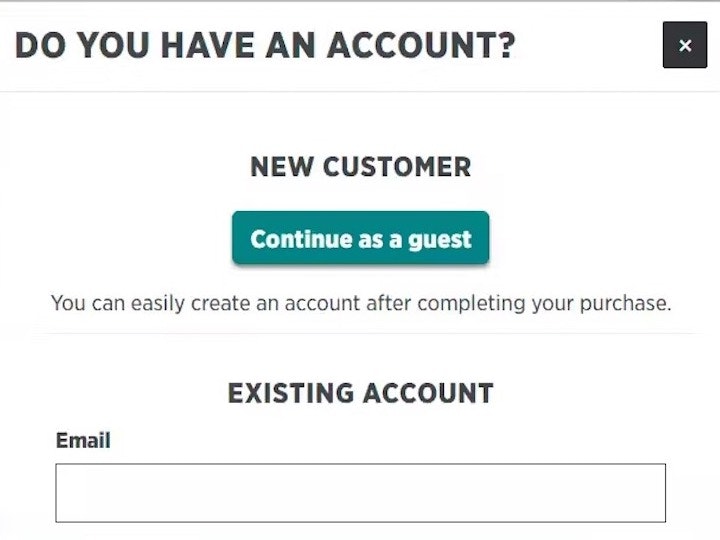

Make “Guest Checkout” the Most Prominent Option (47% Don’t)

January 17, 2023

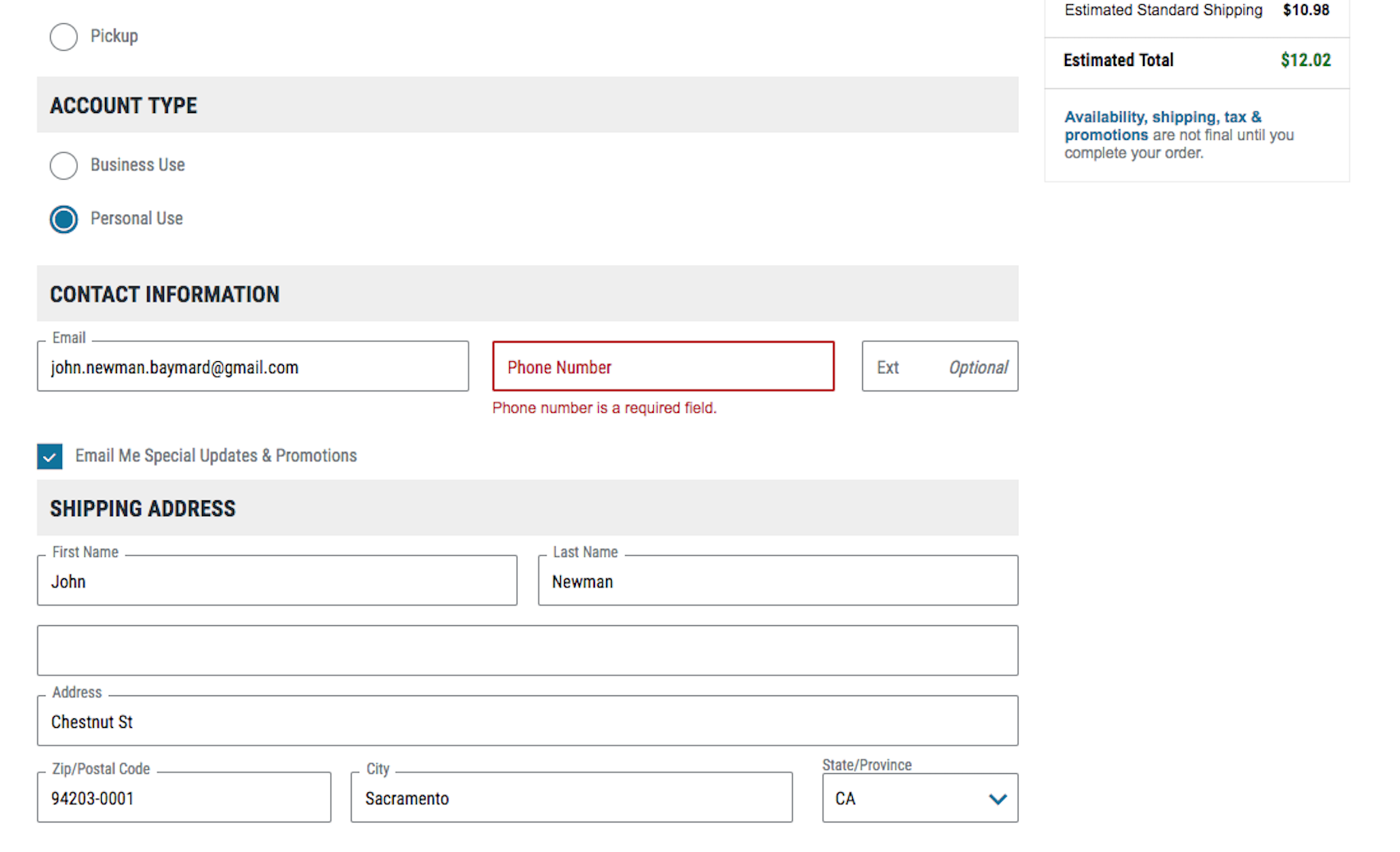

Phone Number UX: Always Explain Why the “Phone Field” Is Required (39% Don’t)

14% of users will abandon checkout if “phone” is simply required. Testing shows users just need an explanation of why the phone field is required — yet 39% of ecommerce sites don’t.

Featured

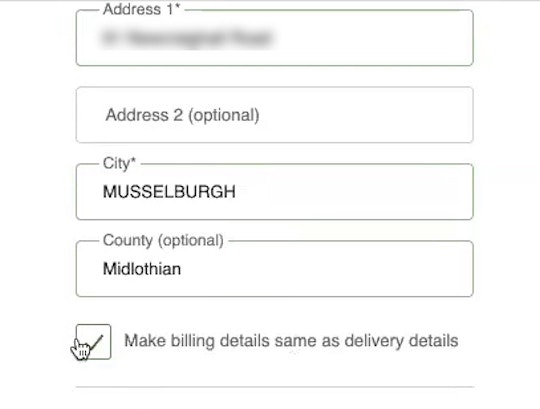

Use “Shipping Address” as “Billing Address” by Default (16% of Mobile Sites Have Implementation Issues)

January 10, 2023

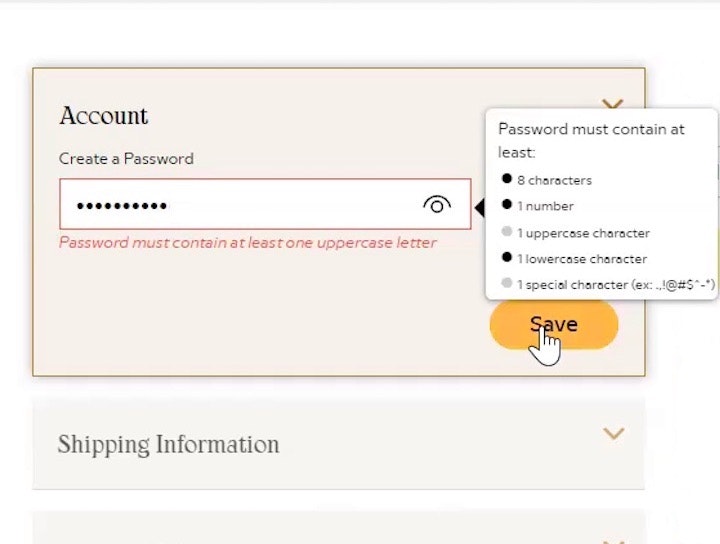

Avoid Unnecessarily Complex Password-Creation Requirements (82% Don’t)

November 29, 2022

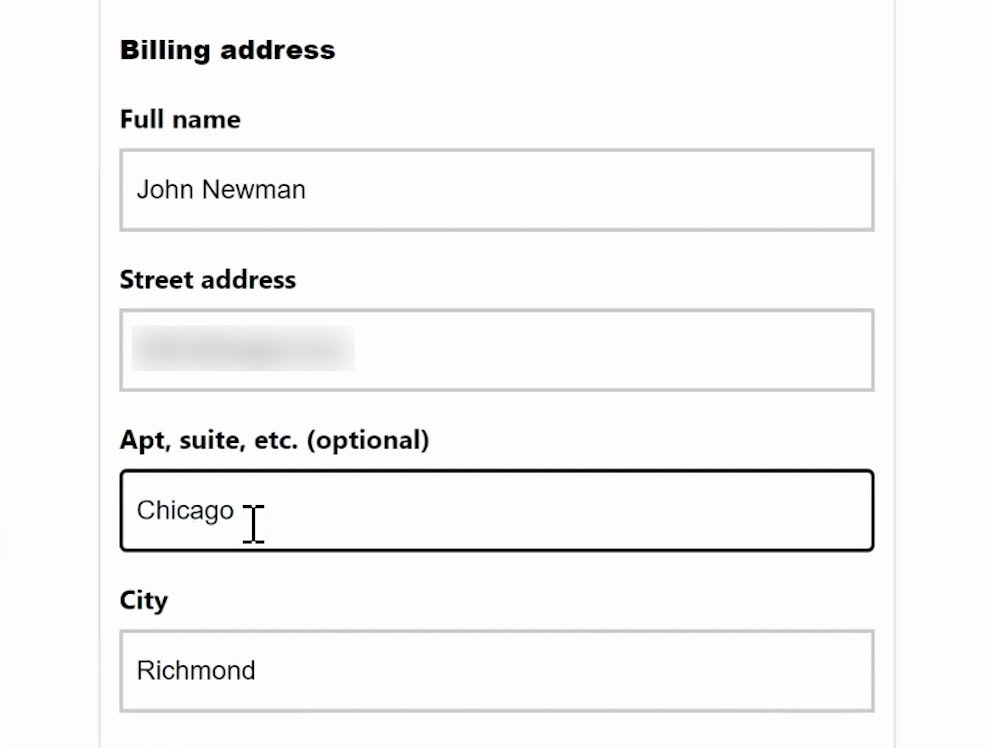

Form Usability: Getting ‘Address Line 2’ Right

October 4, 2022 Popular

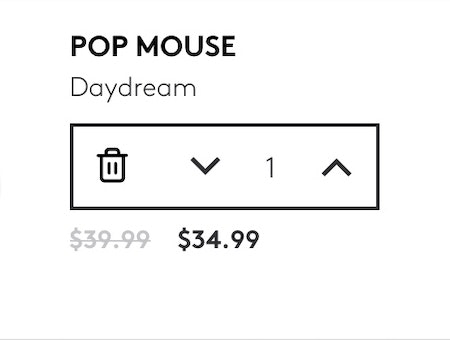

Use Buttons or Buttons Plus an Open Text Field for Updating Cart Quantity (61% Don’t)

September 20, 2022

250+ New Examples Added from Large-Scale Testing on European Sites

November 9, 2021

Baymard Update: 13 New Case Studies and 3 New 2021 Benchmarks (Checkout, Product Page, and On-Site Search UX)

October 12, 2021

6 Ways to Improve the Relevance of Cross-Sells in the Cart (52% of Desktop Sites Don’t Do Enough)

January 12, 2021

4 Design Patterns That Violate “Back” Button UX Expectations – 59% of Sites Get It Wrong

July 20, 2020 Popular

5 ‘Credit Card Form’ Implementations That Make ‘L.L. Bean’ Best-in-Class

June 30, 2020 Popular

5 ‘Order Review’ UX Implementations That Make Office Depot Best-in-Class

July 15, 2019 Popular

Checkout Optimization: From 16 Form Fields to 8 Fields (keynote presentation)

June 21, 2019 Popular

E-Commerce Checkouts Need to Mark Both Required Fields and Optional Fields Explicitly (Only 14% Do So)

October 2, 2018 Popular

CAPTCHAs Have an 8% Failure Rate, and 29% if Case Sensitive

January 18, 2018

Remove Select Features When There’s Only One Option Left (14% Don’t)

December 12, 2017

Consider Using Localized Input Masks for ‘Phone’ and Other Restricted Inputs (64% Aren’t Taking Advantage of Input Masking)

November 28, 2017 Popular

5 Common Usability Pitfalls of Custom Designed Drop-Downs (31% Have Drop-Down UI Issues)

November 14, 2017 Popular

How Users Perceive Security During the Checkout Flow (Incl. New ‘Trust Seal’ Study 2023)

October 5, 2016 Popular

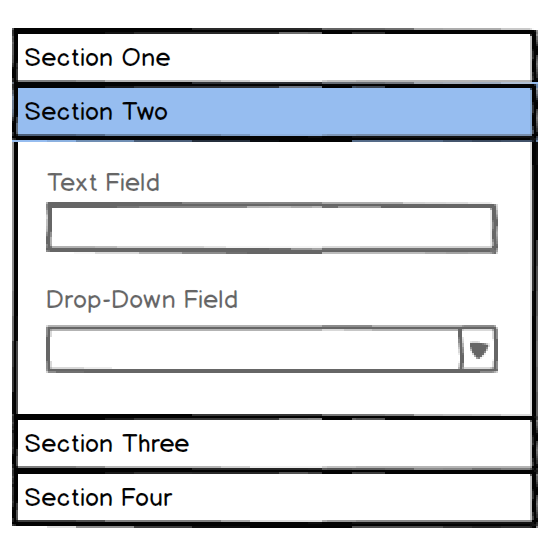

Accordion UX: The Pitfalls of Inline Accordion and Tab Designs

October 21, 2014

Fixing Bugs – the Next ‘Big Thing’ in E-Commerce?

October 7, 2014

Form Usability: Validations vs Warnings

September 23, 2014

How to Recoup 30% of “Card Declined” Abandonments

August 13, 2013

Users Continue to Double-Click Online

July 25, 2013

Which Site Seal do People Trust the Most? (2013/2016 Survey Results)

January 22, 2013

A Holistic View on the Current State of Checkout Usability

November 20, 2012

Add Descriptions To Checkout Form Labels (92% Get It Wrong)

November 6, 2012

Why Your Checkout Process Should Be Completely Linear

October 3, 2012

Accordion Style Checkouts – The Holy Grail of Checkout Usability?

September 18, 2012 Popular

Visually Reinforce Your Credit Card Fields (89% Get it Wrong)

August 21, 2012 Popular

Checkout Experience: Don’t Require Seemingly Unnecessary Information (61% Get it Wrong)

July 31, 2012

A Consistent Shopping Experience With Product Thumbnails

May 22, 2012

Idea: Error-Fields Only

April 10, 2012

Checkout Usability: Apply Changes Immediately and Near the Input

February 22, 2012

Observation: Users Will Go Far to Avoid Repeat Form Errors

July 12, 2011

E-Commerce Copywriting: Returning Customer?

June 28, 2011

Account ‘Sign Up’: Ask to Confirm E-mail, Not Password

June 16, 2011

One Page Checkouts – the Holy Grail of Checkout Usability?

April 26, 2011 Popular

E-Commerce: Why Customers Abandon Their Shopping Cart

January 19, 2011

User Expectations: Create an Illusion of Space

January 7, 2011

Form Field Usability: Matching User Expectations

August 31, 2010

People Think Registration Leads to “Spam”

March 25, 2010

Want to learn more about this topic?

Explore Other Research Content

334 top sites ranked by UX performance.

18,000+ annotated designs for systematic inspiration.

Code samples, demos, and key stats for usability.